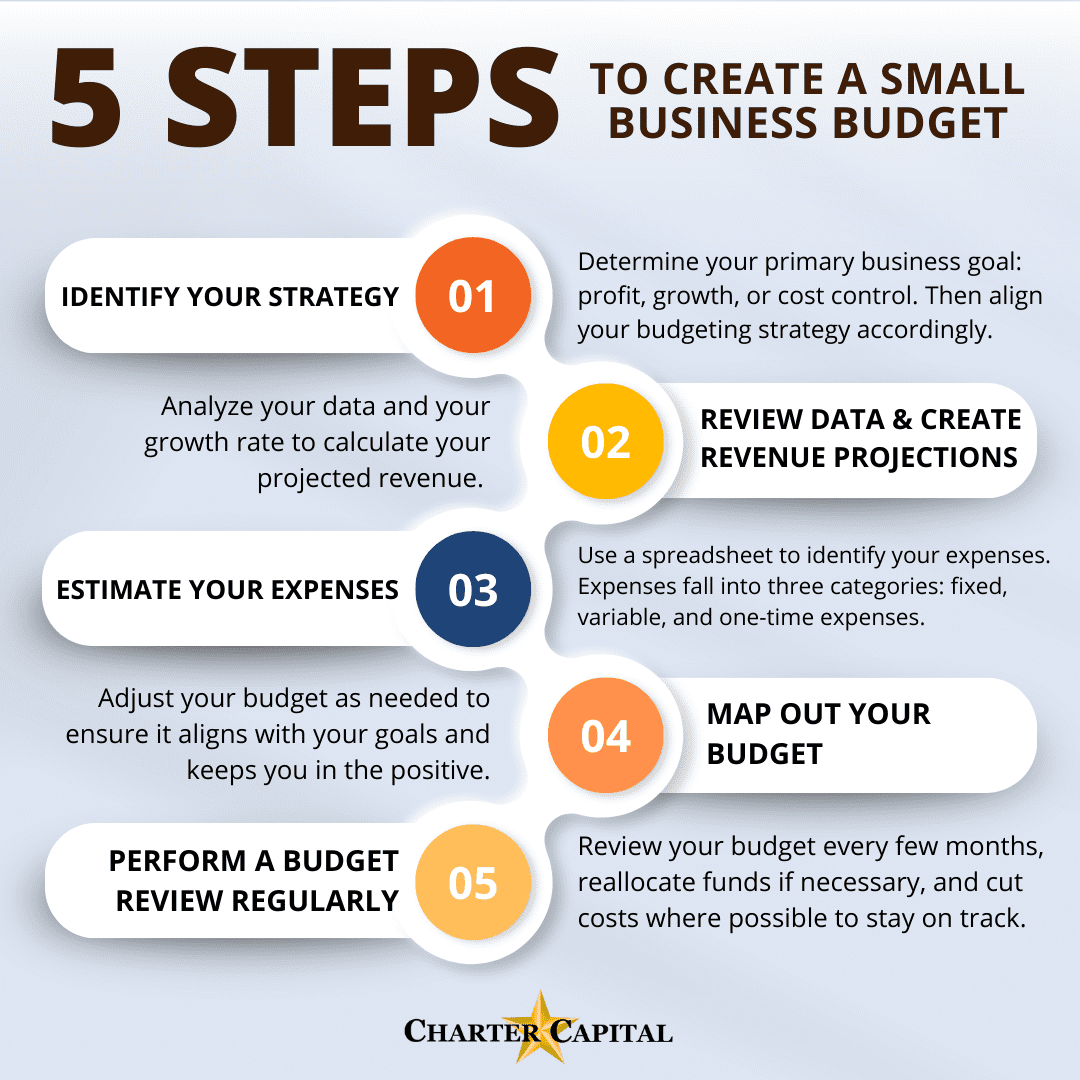

Creating a well-structured budget plan is a crucial step towards achieving financial stability and success. A budget plan serves as a roadmap, guiding individuals and businesses in managing their finances effectively. It enables them to track their income and expenses, identify areas of wastage, and make informed decisions about resource allocation. A effective budget plan helps to prioritize spending, reduce financial stress, and achieve long-term financial goals. By doing so, it lays the foundation for a secure financial future, allowing individuals and businesses to thrive and reach their full potential. Effective budgeting is key to success.

Key Strategies for Creating Effective Budget Plans

To achieve success in any financial endeavor, it is crucial to develop a comprehensive budget plan that accounts for all expenses, revenues, and financial obligations. An effective budget plan serves as a roadmap, guiding financial decisions and ensuring that resources are allocated efficiently. By understanding the importance of budgeting and implementing a well-structured plan, individuals and organizations can better navigate financial challenges and capitalize on opportunities.

Assessing Financial Situation

Assessing one’s financial situation is the foundational step in creating an effective budget plan. This involves a thorough examination of income sources, fixed expenses, debt obligations, and savings goals. By gaining a clear understanding of the current financial landscape, individuals can identify areas for improvement and make informed decisions about resource allocation. A key aspect of this process is to categorize expenses into needs versus wants, allowing for a more nuanced approach to budgeting.

| Expense Category | Description | Monthly Allocation |

|---|---|---|

| Fixed Expenses | Rent, Utilities, Minimum Debt Payments | $1,500 |

| Variable Expenses | Groceries, Entertainment, Travel | $800 |

| Savings | Emergency Fund, Retirement Savings | $500 |

Setting Realistic Financial Goals

Setting realistic financial goals is essential to the success of a budget plan. These goals should be specific, measurable, achievable, relevant, and time-bound (SMART), providing a clear direction for financial efforts. Whether the objective is to reduce debt, build savings, or increase investments, having well-defined goals enables individuals to stay focused and motivated. It is also important to regularly review and adjust these goals as financial circumstances evolve.

| Financial Goal | Target Amount | Timeframe |

|---|---|---|

| Debt Reduction | $10,000 | 12 Months |

| Savings Accumulation | $5,000 | 6 Months |

| Investment Growth | 10% Return | 24 Months |

Monitoring and Adjusting the Budget

Monitoring and adjusting the budget is a critical ongoing process that ensures the plan remains relevant and effective. Regularly tracking expenses and income against the budget allows individuals to identify variances and make necessary adjustments. This might involve reducing spending in certain categories, allocating additional funds to savings or debt repayment, or revising financial goals in response to changing circumstances. By maintaining a proactive approach to budget management, individuals can stay on track to achieve their financial objectives.

Track expenses to control your finances

Track expenses to control your finances| Budget Component | Original Allocation | Adjusted Allocation |

|---|---|---|

| Groceries | $400 | $350 |

| Entertainment | $200 | $150 |

| Debt Repayment | $300 | $500 |

Key Components of a Successful Budget Plan

A well-structured budget plan is crucial for achieving financial stability and success, as it enables individuals and organizations to manage their financial resources effectively, prioritize their expenditure, and make informed decisions about investments and savings.

Assessing Financial Situation

To create an effective budget plan, it is essential to have a clear understanding of your current financial situation, including your income, expenses, assets, and liabilities, which will help you identify areas for improvement and make informed decisions about resource allocation.

Setting Financial Goals

Financial goals should be specific, measurable, achievable, relevant, and time-bound (SMART), and may include objectives such as saving for a major purchase, paying off debt, or building an emergency fund, which will help guide your budgeting decisions and ensure that your financial resources are being utilized effectively.

Prioritizing Expenditure

Effective budgeting requires prioritizing expenditure based on financial goals and needs, rather than wants, and involves allocating resources to essential expenses, such as housing and food, before discretionary spending, such as entertainment and hobbies.

Monitoring and Adjusting

A budget plan is not a static document, but rather a dynamic tool that requires regular monitoring and adjustments to ensure that it remains relevant and effective in achieving financial goals, and involves tracking expenditure, identifying areas for improvement, and making changes as needed.

Use apps to simplify budget management

Use apps to simplify budget managementMaintaining Discipline

Budgeting discipline is critical to achieving financial success, and involves avoiding impulse purchases, minimizing unnecessary expenses, and staying committed to long-term financial goals, even in the face of financial challenges or unexpected expenses.

Frequently Asked Questions

What is the first step in creating an effective budget plan?

The first step in creating an effective budget plan is to track your income and expenses to understand where your money is going. This involves monitoring your financial transactions, including income, fixed expenses, and discretionary spending. By doing so, you can identify areas where you can cut back and allocate resources more efficiently.

How do I prioritize my expenses when creating a budget plan?

To prioritize your expenses, categorize them into needs, wants, and savings. Essential expenses, such as rent, utilities, and food, come first. Next, allocate funds to savings and debt repayment. Finally, consider discretionary spending, such as entertainment and hobbies. Be realistic about your financial goals and adjust your priorities accordingly to ensure a balanced budget.

What are some common budgeting mistakes to avoid?

Common budgeting mistakes include underestimating expenses, failing to account for irregular expenses, and not adjusting for changes in income or expenses. Additionally, not prioritizing needs over wants and failing to review and revise the budget regularly can lead to financial difficulties. By being aware of these potential pitfalls, you can create a more effective and sustainable budget plan.

How often should I review and update my budget plan?

It is essential to review and update your budget plan regularly to ensure it remains relevant and effective. Review your budget at least quarterly, or whenever there are significant changes in your income or expenses. This will help you stay on track with your financial goals, make adjustments as needed, and respond to any unexpected expenses or financial setbacks.

Adjust budgets according to financial changes

Adjust budgets according to financial changes